U.S. Expatriates Are Eligible for Pandemic Relief

Background

The pandemic of Coronavirus COVID-19 has caused widespread disruptions to essential services, business operations, and everyday lives worldwide as governments around the world implement various degrees of quarantine measures in an attempt to contain the contagion.

Recognizing that taxpayers have been adversely affected by the COVID-19 emergency, President Donald Trump first issued an emergency declaration to postpone the due dates of federal income tax returns and making certain tax payments on March 13, 2020. He then signed into law on March 27, 2020 the “Coronavirus Aid, Relief, and Economic Security Act” (the “CARES Act”) shortly after the bill was passed by both houses of Congress with overwhelming support. The CARES Act includes various tax provisions that are designed to support families, workers, and small businesses through these difficult times. In this newsletter, we will review how key aspects of these provisions may apply to you as U.S. expatriates.

I. Federal Income Tax Return Filing and Payment

What is the Filing Due Date for U.S. Expats?

U.S. citizens or residents whose tax homes and abodes, in a real and substantial sense, are outside the U.S. and Puerto Rico on April 15, 2020 may qualify for an automatic two-month extension to June 15, 2020 for the filing of their federal income tax returns provided a statement is attach to the return to establish the eligibility.[1]

Under Notice 2020-18, the due date for filing federal income tax returns is automatically postponed to July 15, 2020. This is more favorable than the automatic two-month extension and there is no need to furnish a statement or file a Form 4868 in order to qualify.

Taxpayers should note that this postponement does not apply to their filing obligations for other types of federal tax or information returns.[2],[3] Expatriates with such obligations should consider filing the applicable extensions (and making timely tax payments) should they require additional time to prepare and file these returns.

Observation: States, however, are not consistently in their approaches. In order to avoid late filing penalty, you should consult the website of your state’s Department of Revenue or Taxation for the latest update.

What is the Tax Payment Due Date for U.S. Expats?

With the automatic two-month extension, late payment penalty is assessed on federal income tax returns only if the balance due is not paid by June 15, 2020 but interest will still accrue from April 15, 2020.

The due date for filing federal income tax payments (including payment of self-employment tax) has also been automatically postponed to July 15, 2020 by Notice 2020-18. Contrary to the initial announcement made by Secretary Mnuchin, there is no limitation on the amount that may be postponed. Interest as well as late payment and late filing penalty will not be assessed during the period of postponement.[2]

What If I Still Need More Time Beyond July 15, 2020 to File My Return?

You can request an automatic extension of time to file your federal income tax return by submitting a Form 4868. A simple and quick alternative is to make an online payment for Form 4868 extension (https://www.irs.gov/payments) to settling all or part of your anticipated balance due using your U.S. bank account or credit/debit card.

Under Notice 2020-18, the request must be submitted by July 15, 2020 even though the usual deadline would have been April 15, 2020 (or June 15, 2020 for expatriates who qualify for the automatic two-month extension). The extended due date will remain October 15, 2020, unaffected by the postponement.[4]

Despite the extension, interest and late payment penalty, if applicable[5], will continue to accrue on any unpaid balance from July 16, 2020.[2],[4]

In order for the extension to be valid, you must properly estimate and indicate your 2019 tax liability, whichever application method you may opt to use and regardless of the amount you choose to pay.[6]

What If I Need Even More Time Because 2019 was My First Year Overseas and I am Waiting to Qualify for Foreign Earned Income Exclusion?

If you anticipate to qualify for foreign earned income exclusion under Physical Presence Test by July 15, 2020, you may rely on Notice 2020-18 to file your federal income tax return and settle any balance due by July 15, 2020.

On the other hand, if you will qualify for the exclusion under Physical Presence Test only after July 15, 2020 but no later than October 15, 2020, you should request an automatic extension as explained above.

In the event you will qualify for the exclusion after October 15, 2020, by either Physical Presence Test or Bona Fide Residence Test, you should apply for an extension with a Form 2350 no later than July 15, 2020. Generally, if you are granted an extension, it will be to a date 30 days after the date on which you expect to meet either the Bona Fide Residence test or the Physical Presence Test. But if you must allocate moving expenses, you may be given an extension up to 90 days after the end of 2020. In case you expect to owe tax, you should consider making a payment with the application in order to avoid interest and late payment penalty, if applicable, from accruing on any unpaid balance starting July 16, 2020.

Does It Mean I Don’t Have to Make Any Federal Quarterly Estimated Income Tax Payments Until July 15, 2020?

No, the second quarter’s estimated income tax payment will still be due on June 15, 2020 as usual.[7] Only the first quarter’s estimated income tax payment due date has been postponed from April 15, 2020 to July 15, 2020.[2] Due dates for making the third and fourth quarters’ estimated tax payments also remain unchanged.

Can IRA Contributions for 2019 Still be Made After April 15, 2020?

Yes, the deadline for making 2019 IRA contributions has, likewise, been postponed to July 15, 2020.[8]

II. Recovery Rebates and Economic Impact Payments

Will U.S. Citizens and Green Card Holders Residing Overseas Be Eligible for Economic Impact Payments?

U.S. expatriates residing overseas are not precluded from receiving economic impact payments (aka stimulus payments). This payment is actually an “advance” of the Recovery Rebate that will be credited against your federal income tax for tax year 2020 (i.e. the return you will file in 2021).[9]

Must I File My 2019 Federal Income Tax Return to Receive the Payment?

No, the IRS will use data from your 2018 federal income tax return to determine your eligibility and amount payable if your 2019 return has not yet been filed prior to the remittance of the payment.[10]

How Much Is the Economic Impact Payment?

The payment to be made will be determined in the same way as Recovery Rebates based on five elements from your 2019 (or, if not yet filed, 2018) federal income tax return:[11]

- Filing status;

- Resident and dependent status of the taxpayer and spouse;

- Adjusted gross income (AGI);

- Qualifying dependents; and

- Social security numbers included on the return[12]

Nonresident aliens and those who could be claimed as a dependent of another taxpayer are not eligible for Recovery Rebates.[13] Neither are resident aliens with social security numbers not authorized for employment or Individual Taxpayer Identification Numbers (ITINs) eligible.[14]

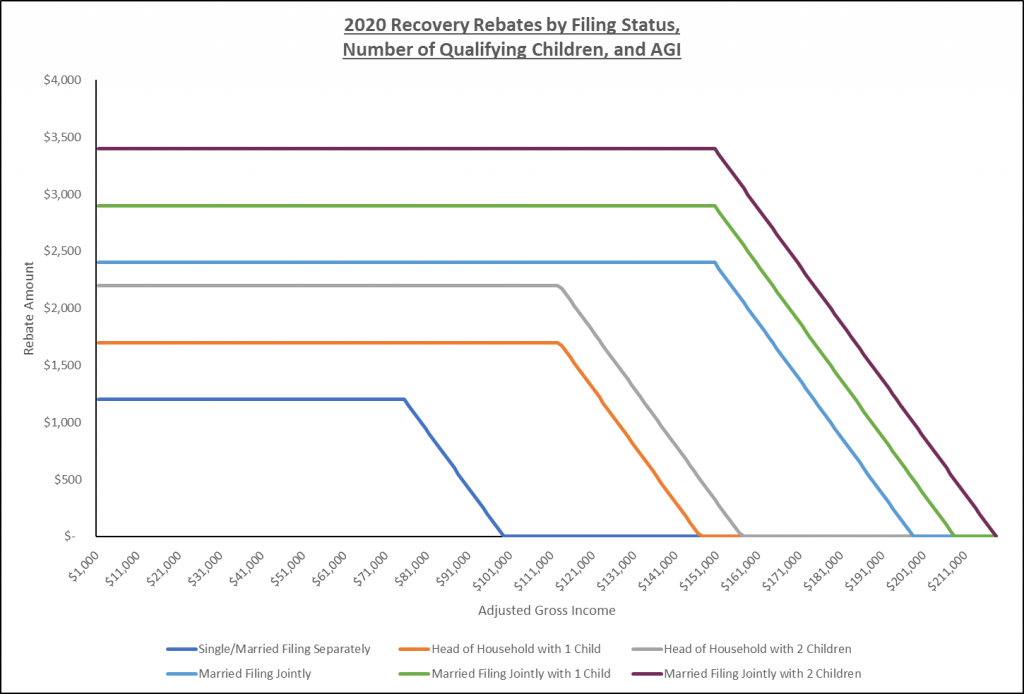

The maximum amounts of payment a taxpayer may receive are as follows:[15]

- Single or Married Filing Separately: $1,200

- Married Filing Jointly: $2,400

- Qualifying Child[16]: $500 each

The payment will be phased out at a rate of 5% for each $1 of AGI above the following thresholds:[17]

- Married Filing Jointly: $150,000

- Head of Household: $112,500

- Single or Married Filing Separately: $75,000

Example 1: Peter is a U.S. citizen and his spouse, Liz, is a green card holder. He has not yet filed a 2019 federal income tax return. On Peter’s 2018 return filed jointly with his spouse, he claimed two dependent children, his 16-year-old daughter and 20-year-old son, a full-time college student, both of whom are U.S. citizens. Peter’s AGI on the 2018 return was $195,000.

The maximum payment for Peter would have been $2,900 ($2,400 for Married Filing Jointly + $500 for one qualifying child). However, his payment will be reduced to $650 ($2,900 - ($195,000 - $150,000) x 5%) because his AGI was above the threshold for taxpayers who filed a joint return.

Below is an illustration of the amount of Recovery Rebate creditable based on filing status, number of qualifying children, and AGI:

Observation: While spouses who are otherwise nonresident aliens but have a valid joint return election in effect may be deemed a resident alien for individual income tax purposes, they will fail to qualify for Recovery Rebates since they will not have been issued a social security number with an authorization for employment.

How Will the Payment be Made to Me?

The IRS will calculate and automatically send the payment to you, provided you are eligible and it is not fully phased out due to your AGI. To expedite payments, the payment will be delivered electronically to any account which you had authorized to receive a tax refund or other federal payment on or after January 1, 2018. Otherwise, paper checks would be issued.[18],[19]

Can I Choose to Receive the Payment Electronically If the IRS Does Not Have My Direct Deposit Information?

Yes. The Treasury Department plans to develop a web-based portal for individuals to provide their banking information to the IRS online, so that individuals can receive payments electronically as opposed to checks in the mail.[19]

Observation: Electronic payment would likely be preferable for expatriates residing overseas or are in the midst of relocation. Note, however, the IRS only accepts U.S. bank accounts for direct deposits.

Will I Receive the Payment If I Am Retired Overseas and Have Not Had a Filing Requirement?

If you are a senior citizen, social security recipients, or railroad retirees who are not otherwise required to file a 2018 or 2019 federal income tax return, the IRS will use the information on your Form SSA-1099 or Form RRB-1099 to compute the payment.[20] Since the IRS would not have information regarding any dependents you may have, $1,200 will be paid without the additional amount for dependents at this time.[19] The payment will be made as a direct deposit or by paper check, just as you would normally receive your benefits.[21]

Observation: If you are not a recipient of social security or railroad retirement benefits, you will not receive any economic impact payment or Recovery Rebate unless you file a federal income tax return for 2018, 2019, or 2020.

How Will I Know How Much I Am to Receive for the Payment?

The IRS will notify you by mail, at the last known address within 15 days of remitting the payment, of the method by which the payment was made, the amount of such payment, and a phone number for the appropriate point of contact at the IRS to report any failure to receive such payment.[22]

Observation: In the event you have moved since filing your last federal income tax return, you should call the IRS Help Desk at 1-800-829-1040 to update your address. Even though the hold time will be longer than usual, this will be more expedient than sending a Form 8822, which generally takes 4 to 6 weeks to process during normal times.

What Happens When I File My 2020 Federal Income Tax Return?

When you file your 2020 federal income tax return in 2021, the credit for Recovery Rebate will be determined based on the same elements explained earlier. If the credit is smaller than the economic impact payment, you will not be required to repay the excess. In contrast, if the credit is greater than the payment, you will be able to claim the difference on your 2020 return.[23]

Example 2: Peter files his 2020 federal income tax return in 2021. Because of a pay cut he took during the year as a result of the pandemic, his AGI for 2020 has dropped to $156,000. His son also managed to land a job after college graduation and was no longer a dependent of his. On the joint return he files with Liz, he claims his 18-year-old daughter as a dependent.

Peter is aware that his 18-year-old daughter is not a qualifying child and calculates that his credit for Recovery Rebate would have been $2,400 for filing jointly with Liz. Since his AGI is above the threshold for joint filers, the credit is reduced to $2,100 ($2,400 - ($156,000 - $150,000) x 5%).

He retrieves his record for the amount of economic impact payment he received in 2020 and finds that it was only $650. Since it is smaller than the credit of $2,100, Peter should expect to receive the difference of $1,450 with the filing of his return.

Example 3: If Peter’s AGI for 2020 was to remain at $195,000 as reported on his 2018 federal income tax return, the credit to be shown on his 2020 return would just be $150 ($2,400 - ($195,000 - $150,000) x 5%). Even though the credit of $150 is less than the $650 he received for economic impact payment, the excess does not need to be repaid to the IRS.

Will the Excess of Payment Over the Credit for Recovery Rebate be Considered Taxable Income?

No. The recovery rebate is not subject to federal income tax. As with any tax refund under the law, the rebate is not treated as income, or as a resource for a 12-month period, in determining an individual's eligibility or assistance amount under any federally funded public program.[24],[25]

III. Other Tax Provisions

Does the CARES Act Include Other Individual Income Tax Provisions?

Yes, CARES Act also includes the following provisions:

- Deduction for Charitable Contributions:

- Above-the-Line Deduction: Taxpayers who do not itemize deductions may deduct up to $300 in cash contributions made to certain qualified charitable organizations, beginning in tax year 2020[26]; and

- Temporary Suspension of Limitation: Taxpayers who itemize deductions may deduct up to 100% (in lieu of 60%) of their AGI for cash contributions made to certain qualified charitable organizations during tax year 2020.[27]

Observation: With a vast majority of taxpayers taking standard deduction under Tax Cuts and Jobs Act (TCJA), the new above-the-line deduction for charitable contributions, which is not limited to tax year 2020, should provide many taxpayers a modest tax benefit from charitable giving. Expatriates should be aware that charitable contributions to foreign organizations do not generally qualify for deductions and should consult the Tax Exempt Organization Search to determine whether an organization is qualified for purposes of charitable contribution deduction.

- Special Rules for Use of Retirement Funds: The following reliefs are made available to taxpayers[28]:

- who are diagnosed with SARS-CoV-2 or Coronavirus by a test approved by the Centers for Disease Control and Prevention;

- whose spouse or dependent is diagnosed with such virus or disease by such a test; or

- who experience adverse financial consequence as a result of:

- being quarantined, furloughed, or laid off;

- having work hours reduced due to such virus or disease

- being unable to work due to lack of child care because of such virus or disease;

- closing or reducing hours of a business owned or operated by the individual due to such virus or disease; or

- other factors as determined by the Secretary of the Treasury.

- Certain Tax-Favored Withdrawals from Coronavirus-Related Withdrawals[29]: Taxpayers may, within tax year 2020, withdraw up to $100,000 and such withdrawals will not be subject to the 10% early withdrawal penalty. Any taxable income from these withdrawals will be included on the taxpayer’s returns ratably over three tax years, starting 2020, unless the taxpayer elects otherwise. Amounts withdrawn may also be repaid within three years without regard to annual contribution limits, in which case, amounts repaid will be treated as a 60-day rollover and not be subject to tax.

- Loan from a Qualified Employer Plan[30]:

- Maximum Loan Amount: The maximum amount a taxpayer may borrow, on a loan made within 180 days beginning March 27, 2020 (the enactment date of CARES Act), is increased to the lesser of:

- 100% (from 50%) of the vested account balance or $10,000; or

- $100,000 (from $50,000)

- Maximum Loan Amount: The maximum amount a taxpayer may borrow, on a loan made within 180 days beginning March 27, 2020 (the enactment date of CARES Act), is increased to the lesser of:

- Delay of Repayment on an Outstanding Loan: Any repayment for such loan that would otherwise be due between March 27, 2020 and December 31, 2020 will be delayed for 1 year. Subsequent repayments will be adjusted to reflect the delay and interest accrued during such delay and the 5-year repayment period will be extended.

Observation: These provisions allow taxpayers to draw on retirement funds in times of financial difficulties but avail taxpayers some flexibility in "reinvesting" such withdrawals into these plans at a later time.

- Temporary Waiver of Required Minimum Distribution (RMD) Rules for Certain Retirement Plans and Accounts[31]:

- General Rule: RMD from various defined contribution plans as well as traditional and ROTH IRAs for calendar year 2020 will be waived regardless of whether the taxpayer experienced adverse financial consequences as a result of the pandemic.

- Taxpayers Whose First RMD Starts in 2020: Taxpayers who delayed their first RMD from 2019 to 2020 will also be eligible for the waiver.

- Retirement Accounts Inherited from Decedents: Calendar year 2020 may be disregarded for purposes of applying the 5-year rule to a retirement account that was inherited from a decedent.

Observation: These provisions allow taxpayers to conserve their assets without needing to liquidate them at a time when the value may have been negatively impacted due to the pandemic.

[1] Treas. Reg. Sec. 1.6081-5

[2] Notice 2020-18, Section III

[3] Filing and Payment Deadlines Q&A3, 7, and 10

[4] Filing and Payment Deadlines Q&A12

[5] Failure to pay penalty not applicable provided at least 90% of the tax liability is paid by the regular due date and the balance is settled with the return pursuant to IRC Sec. 301.6651-1(a)(2) and (c)(3)

[6] Form 4868 filing instructions and Treas. Reg. Sec. 1.6081-4(b)(4)

[7] Filing and Payment Deadlines Q&A16

[8] Filing and Payment Deadlines Q&A17

[9] IRC Sec. 6428(e) and (f)

[10] IRC Sec. 6428(f)(5)(A)

[11] IRC Sec. 6428(f)(2)

[12] Adoption taxpayer identification number also acceptable. IRC Sec. 6428(g)(2)(B)

[13] IRC Sec. 6428(d)

[14] IRC Sec. 6428(g)(2)(A) and 24(h)(7)

[15] IRC Sec. 6428(a)

[16] Qualifying child is a dependent of the taxpayer, who is under the age of 17, and must be a U.S. citizen, national, or resident. IRC Sec. 6428(a)(2) and 24(c)

[17] IRC Sec. 6428(c)

[18] IRC Sec. 6428(f)(3)(B)

[19] IR-2020-61

[20] IRC Sec. 6428(f)(5)(B)

[21] Treasury News Release, April 1, 2020

[22] IRC. Sec. 6428(f)(6)

[23] IRC Sec. 6428(e)(1)

[24] IRC Sec. 6409

[25] “COVID-19 and Direct Payments to Individuals: Will Social Security and Supplemental Security Income Beneficiaries Receive the Recovery Rebate in the CARES Act?”, Congressional Research Service (Updated April 2, 2020)

[26] IRC Sec. 62(a)(22)

[27] CARES Act, Sec. 2205

[28] CARES Act, Sec. 2202(a)(4)(A)(ii)

[29] CARES Act, Sec. 2202(a)

[30] CARES Act, Sec. 2202(b)

[31] CARES Act, Sec. 2203

American Expatriate Tax is a part of Contexo Global Mobility Solutions & Tax Consulting Ltd. registered in Hong Kong. Together, we help companies and individuals navigate through the complexities of global mobility and related tax issues. Here is where you will find a blend of expertise from Big 4 accounting firms and Fortune Global 500 companies but the attention of a boutique consulting practice. The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.